Summarize this article with

As 2024 approaches, it is a time for reflection and anticipation. This year, we're focusing on the upcoming advancements in financial technology. We've identified the top three trends that will gain prominence in 2024.

A common theme across these trends is the ongoing democratization and transparency in consumer purchasing and personal wealth management. Consumers increasingly want control over their financial power, the ability to use their money when and how they wish, and 24/7 access to their financial services through websites or mobile browsers without human interaction.

The trends discussed below reflect this industry shift in their growing popularity and demand.

Trend 1: The expansion of open banking APIs

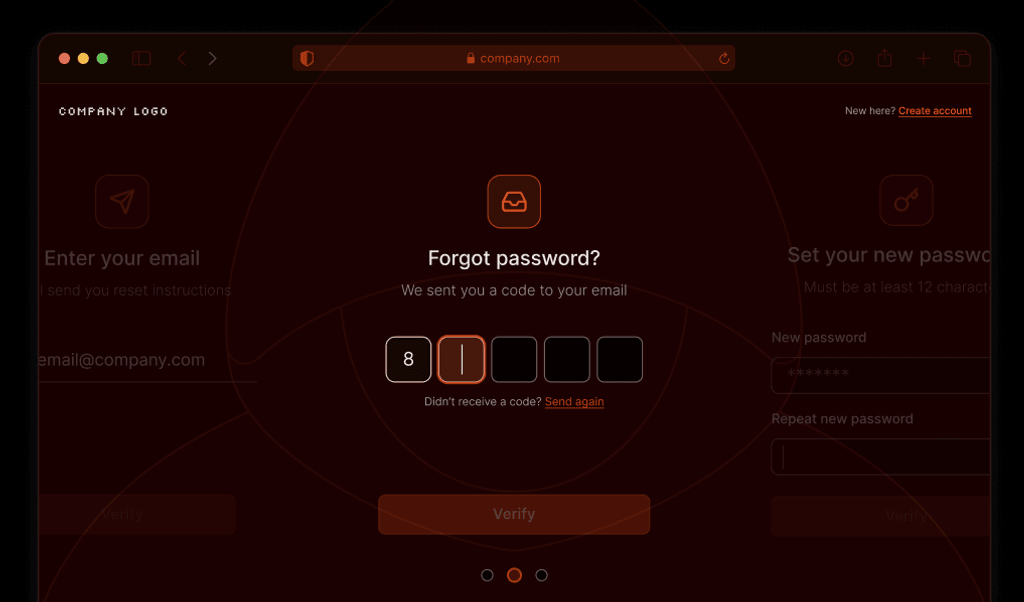

We've explored the concept of open banking APIs and their role in enhancing consumer transparency and convenience. They support third-party financial applications like Venmo and Mint and promote data-sharing and collaboration. Open banking allows customers to access a broad range of custom-made financial services.

Increased competition in this area encourages innovation, creating personalized financial management apps, streamlined loan approvals, and real-time payment systems. We anticipate a continued rise in demand for these services next year, enabling consumers to access better and understand their financial health and data.

However, open banking also brings potential risks, such as fraudulent account linking, involving unauthorized connections between financial accounts and third-party applications orchestrated by fraudsters.

We've emphasized the need for fraud prevention in open banking. Measures such as real-time transaction monitoring and robust identity verification protocols can help mitigate these risks.

Trend 2: Buy Now, Pay Later (BNPL) as a direct competitor to credit cards

BNPL has gained popularity over the past few years as eCommerce's answer to in-store layaway plans of the past. With Buy Now Pay Later, consumers can "pay in four" or over time for purchases of all sizes, from just a few dollars on sites like Sephora to more considerable purchases like Peloton and furniture.

In 2021, 17% of consumers with a credit card used BNPL service on average, and some of the most popular providers like Affirm and Afterpay captured almost a ⅓ of the BNPL market each, according to Bankrate. Additionally, in 2023, the Wall Street Journal reported that consumers were choosing to purchase more everyday items, such as groceries, through BNPL providers since these smaller, short-term loans were not included on typical credit reports, whereas buying the same things with a credit card would reflect on their credit report.

We're expecting to see a transition of BNPL becoming the preferred payment method for consumers looking for cash and debit alternatives for all sizes of purchases—from cosmetics to couches, potentially for even larger purchases, such as vehicles in the future.

BNPL providers must remain aware and vigilant about potential fraud attacks such as credential stuffing and account takeover of their systems. With high-accuracy device identification, providers can prevent fraud and increase approval rates without adding clunky identity verification steps.

Trend 3: Mobile payment as the only or preferred option

In the past year, you've likely purchased at a major retailer without physically opening your wallet, opting to pay via your mobile device. This means you've completed your transaction with a finger tap, facial recognition, or by tapping your mobile device.

Mobile payments have surged in usage and now account for over half of America's most-used payment method compared to traditional wallets. The benefits of mobile payments are clear: fast and easy access to digital payment cards with no need for physical copies at establishments offering tap-to-pay or one-click online checkout.

However, digital wallets can introduce new types of risks, such as unauthorized access to digital cards without additional identity verification. Fraudsters can target consumers through email phishing, social engineering, and data breaches. Some digital cards, such as Apple Card's Advanced Fraud Protection offer advanced security features such as a rotating security code and tokenized card numbers when coupled with Apple Pay.

We anticipate the trend of digital wallets and mobile payments to become more widespread than physical wallets, which are easily lost or stolen. Therefore, consumers and financial payment providers will need to adopt preventative measures to protect their data.

Conclusion

In conclusion, open banking APIs, Buy Now, Pay Later services, and mobile payments are three key trends shaping the financial industry's future. While these trends offer unparalleled convenience and innovation, addressing the associated risks, especially fraud prevention and data security, is essential. By implementing advanced visitor identification methods and robust prevention measures, consumers and financial institutions can navigate these trends safely and securely.